FOV Robotics Market Map 2026: A Guide to the European Landscape

A field guide to where robotics is being deployed across Europe, why each sector matters, and how the enabling technology stack underneath makes it all possible.

Petri Rajahalme, Sointu Karjalainen, Dave Haynes & David Ripert

March 19, 2026

We built this European robotics landscape to map where the next generation of physical AI companies are being built - and why Europe has genuine advantages in making it happen.

Europe leads in industrial robotics, surgical systems, and precision automation. German companies dominate factory floor automation. Swiss precision robotics sets global benchmarks. The UK produces surgical robotics competing directly with US incumbents. Built on decades of manufacturing heritage, engineering standards, and university research now accelerating into commercial deployment.

At FOV Ventures, we see robotics as part of a broader "beyond screens" paradigm where spatial computing, AI, computer vision, and edge computing converge to enable machines that perceive and interact with the physical world. Technologies originally built for mapping human environments (XR, vision, foundation models) are now the foundation for robots operating in unstructured, real-world settings.

The companies on this map are building at that intersection.

This is a collaborative map - contribute companies, corrections, or updates here.

The landscape is organised in two layers.

At the top are twelve application verticals - where robots are actually being deployed, the industries being transformed, and the problems being solved.

Underneath sits the enabling stack: hardware components, software infrastructure, and intelligence systems that make those applications possible. Innovation flows upward through this stack. Better sensors enable better perception; better perception enables more capable autonomy; more capable autonomy unlocks deployment environments that were previously out of reach.

Understanding both layers - and how they connect - is essential for understanding where the real opportunity lies.

Scope & Approach: This report maps out the European robotics startup landscape and proposes a taxonomy by application domains and enabling technology layers. We focus on startups (privately-held companies, typically early to growth-stage) and exclude large corporates or public companies, except for a few we consider “European champions.” It is not a comprehensive list and the decision to include which companies is a subjective one. Feel free to reach out to us if you’d like to make sure you’re included.

Market Map Contents

Building in any of these areas? We'd love to hear from you - and if you're in London on 25 March, join us at Vantage Point: Robotics Edition, our investor summit and startup showcase for Europe's frontier robotics founders. Register here.

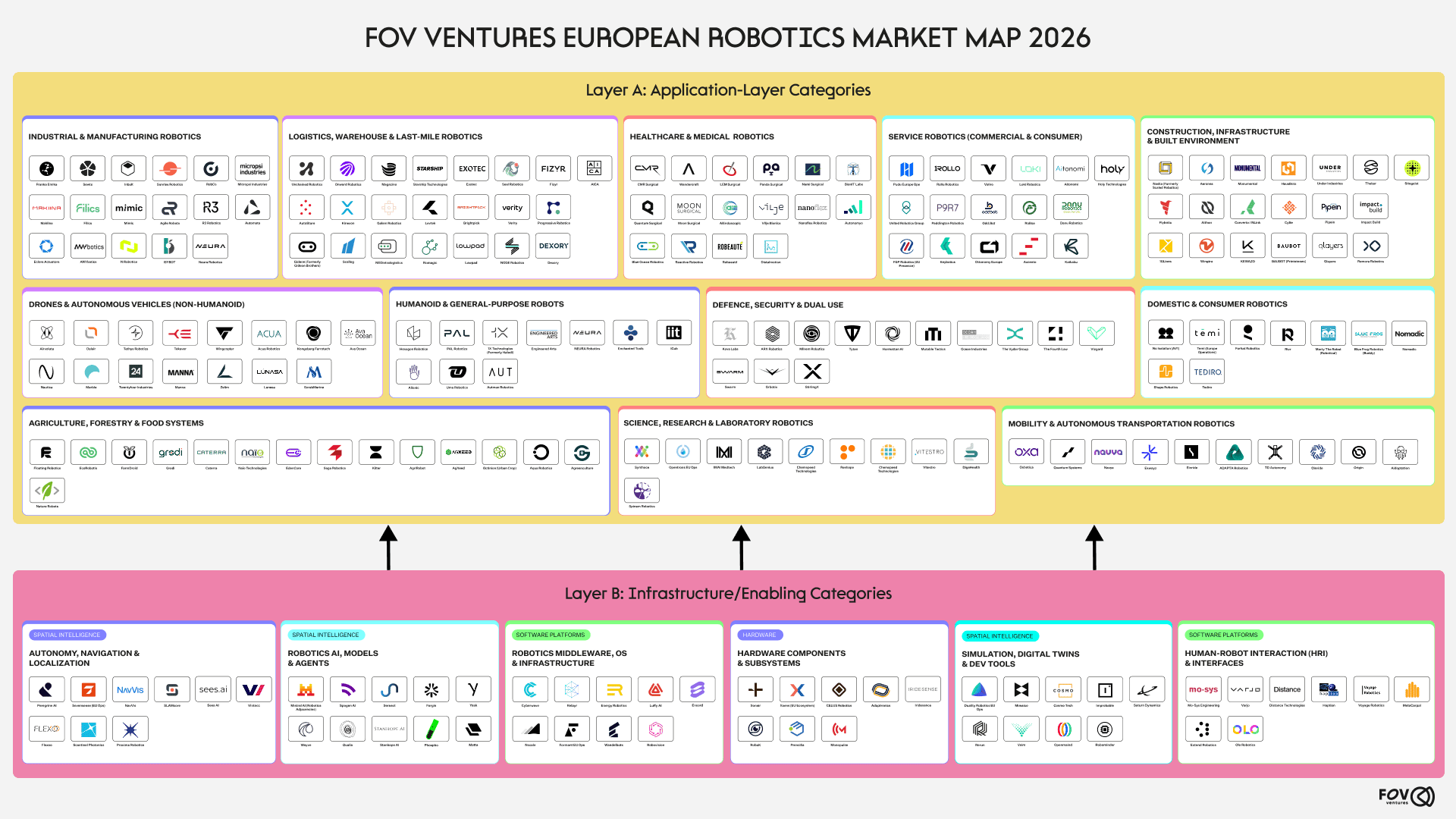

Layer A: Applications

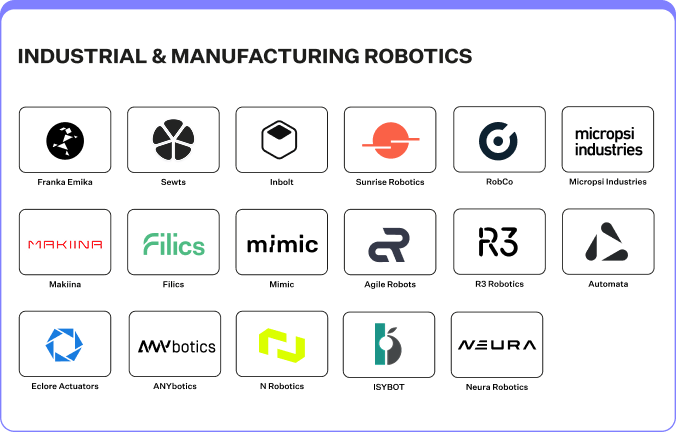

A1. Industrial & Manufacturing Robotics

Europe's manufacturing base is one of its most significant competitive advantages in robotics - and one of its most urgent deployment environments. Germany alone has 429 industrial robots per 10,000 workers, one of the highest densities in the world, and the continent's SME-heavy manufacturing sector creates constant demand for more flexible, more affordable automation. The frontier has moved beyond rigid, single-purpose industrial arms toward collaborative robots that work alongside humans, AI-powered systems that handle variation across SKUs, and no-code programming platforms that let operators retrain robots without external expertise. For the majority of European manufacturers running high-mix, low-volume operations, this flexibility is the unlock that makes automation viable for the first time.

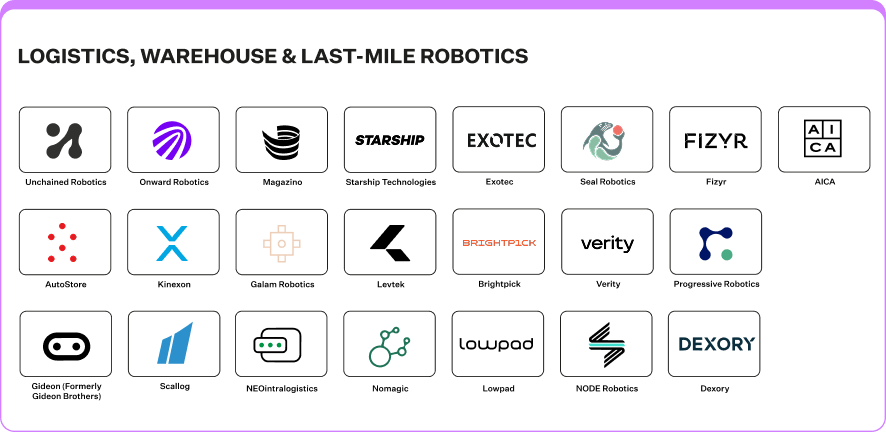

A2. Logistics, Warehouse & Last-Mile Robotics

Logistics was one of the earliest commercial beachheads for robotics in Europe and remains one of the most active. The continent produced some of the world's first warehouse robotics unicorns and continues to attract significant investment across autonomous mobile robots, robotic picking, yard automation, and last-mile delivery. The frontier has shifted to harder problems - unstructured environments, mixed SKU picking, and the genuine complexity of last-mile delivery in European urban settings. As e-commerce volumes grow and warehouse labor tightens, the ROI case only strengthens. Europe's strength here is in systems integration: combining hardware, software, and operational know-how into deployments that actually scale.

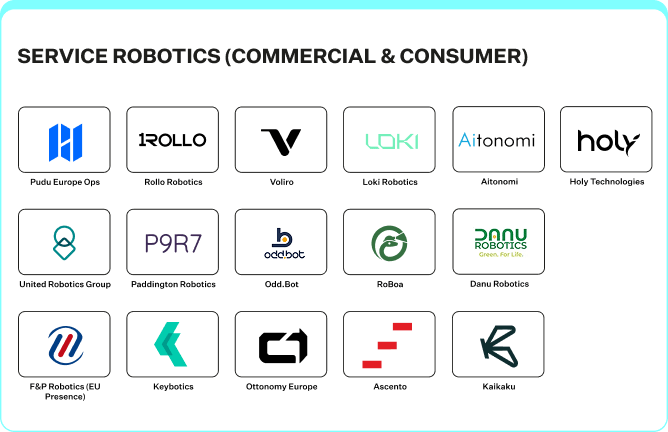

A3. Service Robotics

Service robotics covers a wide range of commercial and consumer deployments - cleaning, security, hospitality, retail - unified by the challenge of operating safely in unpredictable, human-populated environments. Traction has been strongest in cleaning and security, where the operational domain is more bounded and the labor economics are clearest. Hospitality and retail deployments are growing, particularly in high-wage markets where staff turnover is a persistent problem. The form factor that wins in this category is typically one that solves a clear, repeatable operational friction - not one that showcases technical sophistication for its own sake.

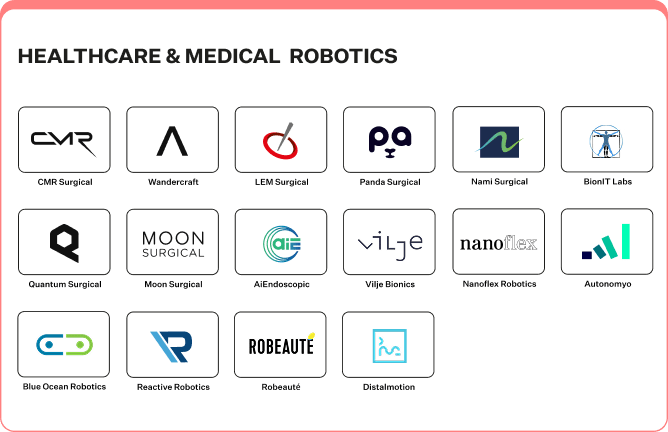

A4. Healthcare & Medical Robotics

Europe's ageing demographics make healthcare robotics less an opportunity and more a necessity. The continent has produced genuine global challengers in surgical robotics, alongside a strong ecosystem in rehabilitation exoskeletons, hospital logistics, and assistive devices. The regulatory environment is demanding - CE marking, clinical validation, long procurement cycles - which acts as both a barrier and a moat. Companies that earn clinical trust early build durable competitive positions. The most accessible near-term opportunity is in hospital operations: disinfection, supply logistics, room turnaround, where ROI is demonstrable and the regulatory burden is lower than in surgical settings.

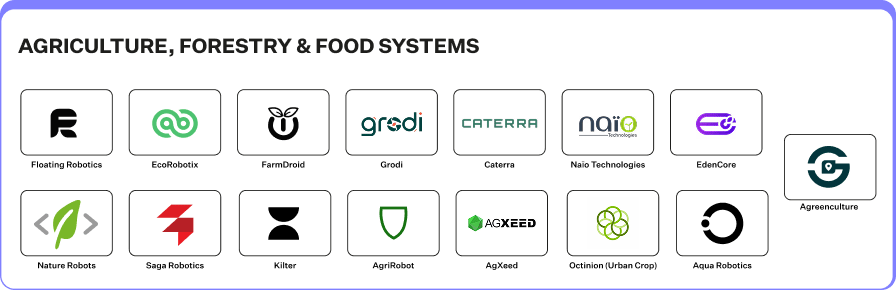

A5. Agriculture, Forestry & Food Systems

European agriculture is under compound pressure: labor shortages, climate volatility, sustainability mandates, and thin margins. Robotics is being applied across the full value chain - autonomous weeding and spraying, precision harvesting, crop monitoring, and indoor farming. Europe's diversity of agricultural contexts - large arable operations in France and the Netherlands, specialty horticulture in Spain and Italy, smaller mixed farms across Scandinavia - provides an unusually rich testing ground. The sustainability angle is particularly strong: precision robotics that reduce chemical inputs and cut fuel consumption align directly with EU agricultural policy, creating regulatory tailwind alongside commercial pull.

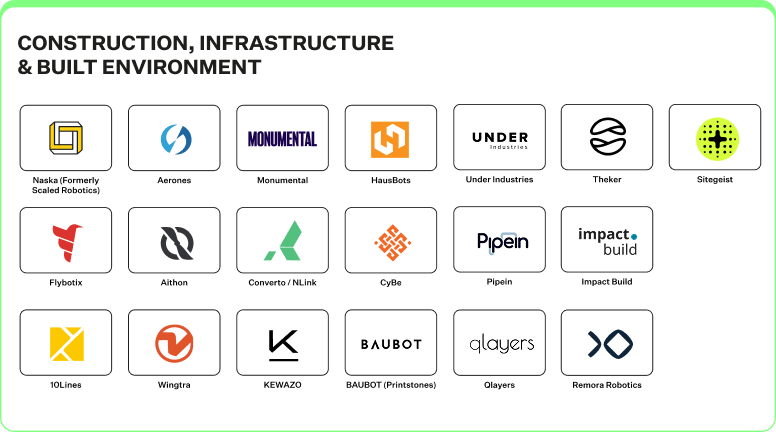

A6. Construction, Infrastructure & Built Environment

Construction is among the least automated industries on earth, and Europe's startup ecosystem is beginning to address that seriously. The sector loses enormous value to delays, rework, and labor gaps - all areas where robotics can help. Early traction has come from well-defined sub-tasks: autonomous site monitoring, scaffolding material handling, precision drilling, infrastructure inspection. Europe's large infrastructure pipeline - offshore energy, housing, transport - creates sustained demand. The constraint is deployment complexity: construction sites are among the most unstructured environments any robot navigates, which is why the most traction starts in bounded, repeatable tasks.

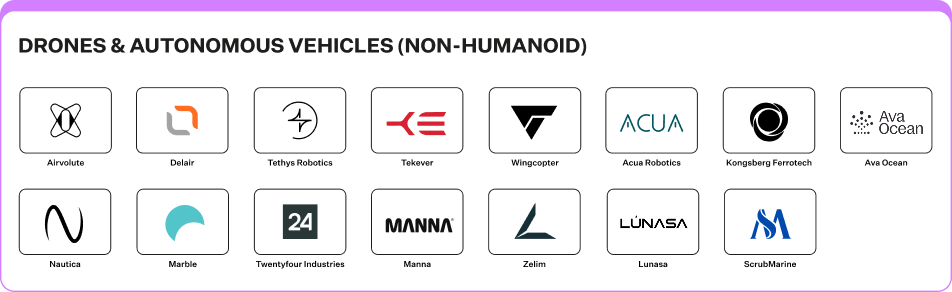

A7. Drones & Autonomous Vehicles

This category spans three distinct but related domains: aerial robotics (drones and UAVs), maritime and underwater systems, and autonomous ground vehicles outside warehouse settings. Europe has particular strength in the first two. Defense and industrial drone capability is well-established, with companies in Germany, Portugal, and the Nordics building serious dual-use platforms. Maritime and underwater robotics is a category where European infrastructure need is acute - North Sea energy assets, rapidly expanding offshore wind, and major port operations all create sustained demand for autonomous inspection and monitoring. Regulatory frameworks for drone operations are also maturing faster in Europe than in many other markets, which is beginning to unlock commercial scale.

A8. Humanoid & General-Purpose Robots

Humanoids are attracting the most attention in robotics, and warrant the most scrutiny on timelines. The commercial logic is real: a robot that operates in human-designed environments without costly retrofitting has a vast addressable market. Europe's contribution here is grounded in deep research heritage - from Italy's iCub to ETH Zurich's locomotion work - increasingly making its way into commercial products. The near-term opportunity is most likely in structured industrial environments where the form factor advantage is genuine. Full general-purpose capability in unstructured settings remains a longer-horizon problem, and the companies most likely to get there are those with the strongest foundation in manipulation and locomotion research.

A9. Defence, Security & Dual Use

Defence is one of the verticals where Europe has moved fastest, driven by genuine urgency. Spending has accelerated across the continent, and with it the demand for autonomous surveillance, ISR drones, unmanned ground vehicles, and dual-use platforms that serve both military and civilian markets. The dual-use nature of the underlying technology - perception, edge compute, secure communications - means that defence robotics and civilian robotics share a stack, and founders who understand both markets have a structural advantage. Europe's defence robotics ecosystem is strongest in the Nordics and Baltics, Germany, and the UK, and is attracting increasing institutional capital alongside government procurement.

A10. Mobility & Autonomous Transportation Robotics

Europe has meaningful technical depth in autonomous vehicle software, and growing deployment in specific mobility contexts: autonomous yard trucks, campus shuttles, port logistics, and sidewalk delivery robots. Full open-road autonomy remains a long-horizon problem, but constrained environments with clear commercial use cases are seeing real traction. EU cross-border regulatory frameworks are beginning to align with deployment ambitions - a meaningful enabler for companies operating across multiple national markets. The most defensible near-term positions are in defined operational domains where the environment is structured enough to make the economics work today.

A11. Science, Research & Laboratory Robotics

Laboratory automation is a less visible but commercially significant category, with strong European presence. Life science research, drug discovery, and materials science all involve highly repetitive, precision-dependent workflows that are well-suited to robotic automation - and where automation genuinely accelerates outcomes rather than simply reducing cost. The AI-driven lab is an emerging concept: robots that don't just execute predefined protocols but can adapt experimental workflows based on real-time results. Europe's strength in biotech and chemistry research creates natural demand, and the category benefits from shorter sales cycles and clearer ROI than many other application verticals.

A12. Domestic & Consumer Robotics

Consumer robotics has historically been a difficult commercial category, but the underlying technology is improving faster than ever. Home robots, companion devices, and educational platforms are being revisited with more capable AI, better manipulation, and more realistic price points. Europe's contribution has been strongest in educational robotics and social assistive devices - products designed around genuine human need rather than technical spectacle. The form factor that wins in consumer markets is one that solves a clear daily friction at a price consumers will actually pay, which remains a harder problem than it looks.

Layer B: The Enabling Stack

Every application above depends on a set of underlying capabilities that determine what robots can actually do, how reliably, and at what cost. This is where the foundational innovation happens - and where European technical heritage is deepest. The stack runs from physical hardware at the base to intelligence at the top, with each layer enabling the one above it.

B1. Robotics AI, Models & Agents

At the top of the enabling stack sits intelligence: foundation models for robotics, spatial AI, perception systems, and the planning and control algorithms that let robots handle real-world complexity. This is where the influence of large language models and vision-language models is being felt most directly in robotics - enabling robots to generalise across tasks rather than being explicitly programmed for each one. It is also where European sovereignty considerations are sharpest. Foundation models trained on industrial data from European factories, with European safety and regulatory standards built in, are a meaningfully different product from those developed elsewhere. The research institutions producing this work - ETH Zurich, TU Munich, INRIA, Oxford - sit at the frontier, and the rate at which that research is converting into commercial products is accelerating.

B2. Simulation, Digital Twins & Dev Tools

Simulation is increasingly central to how robots are developed and trained. Rather than running every experiment in the real world - expensive, slow, and often dangerous - developers use simulators to test robot behaviour across thousands of scenarios, generate synthetic training data, and validate deployments before they happen. Digital twins of specific environments allow companies to replicate real-world conditions at scale. Europe's gaming and real-time rendering heritage feeds directly into this layer: the same capabilities that built world-class 3D engines are now being repurposed as the development infrastructure for robotics.

This layer covers the core capabilities that let robots move intelligently through the world: SLAM (simultaneous localisation and mapping), sensor fusion, motion planning, and fleet autonomy stacks. It's where a significant portion of European robotics IP is concentrated, particularly in vision-based approaches that reduce dependence on expensive infrastructure like GPS or pre-mapped environments. The companies building here often have deep roots in academic research - and the ones that have solved hardware portability and real-time calibration challenges are able to deploy across a much wider range of robot configurations and environments.

B4. Human-Robot Interaction & Interfaces

As robots move into environments shared with humans, the interfaces between people and machines become increasingly important. This category covers teleoperation systems, XR interfaces (augmented and mixed reality), gesture and voice interaction, and haptic feedback. Europe has particular strength here, with a heritage in display technology, optics, and human-computer interaction research that translates directly into robot interface design. The quality of human-robot interaction is often the determining factor in whether a deployment actually gets used - and used safely.

B5. Robotics Middleware, OS & Infrastructure

Above the hardware sits the software infrastructure that makes robots operable at scale: robot operating systems, fleet management platforms, cloud and edge robotics infrastructure. This layer matters particularly for European deployments, which frequently span multiple countries, regulatory environments, and languages. Fleet management platforms that coordinate robots across a French warehouse and a German distribution centre, and OS layers that abstract hardware complexity, are the picks and shovels of the robotics buildout - less glamorous than the applications above, but essential to scaling them.

B6. Hardware Components & Subsystems

At the base of the stack sits hardware: sensors, actuators, end-effectors, power systems, and custom silicon. This is where European optics, photonics, and precision engineering heritage is most directly applicable. LiDAR, vision systems, force-torque sensors, and compliant actuators are all becoming cheaper and more capable - and the companies building robot-native hardware components are often the least visible but most structurally important players in the ecosystem. Cost reduction here is what makes entire application categories commercially viable.

In conclusion, Europe’s robotics startup landscape in 2026 is dynamic and promising, with activity across all layers of the value chain. It offers a fertile hunting ground for investors who share FOV’s vision of the next computing platform being rooted in the physical world, a world where intelligent robots, enabled by spatial computing and AI, augment human productivity in every domain.

Europe has the talent, market demand, and increasingly the capital to build global robotics leaders. With a strong thesis guiding investment (the convergence of spatial computing and robotics) and by leveraging Europe’s collaborative framework, we are confident that the coming years will see many of these startups thrive – delivering returns for investors and strategic value for partners, and quite literally transforming how we live and work through robotics.

Building in any of these areas? We'd love to hear from you - and if you're in London on 25 March, join us at Vantage Point: Robotics Edition, our investor summit and startup showcase for Europe's frontier robotics founders. Register here.